TAX POLICY

The other option available for balancing the budget is to increase revenue. All governments must raise revenue in order to operate. The most common way is by applying some sort of tax on residents (or on their behaviors) in exchange for the benefits the government provides (Figure). As necessary as taxes are, however, they are not without potential downfalls. First, the more money the government collects to cover its costs, the less residents are left with to spend and invest. Second, attempts to raise revenues through taxation may alter the behavior of residents in ways that are counterproductive to the state and the broader economy. Excessively taxing necessary and desirable behaviors like consumption (with a sales tax) or investment (with a capital gains tax) will discourage citizens from engaging in them, potentially slowing economic growth. The goal of tax policy, then, is to determine the most effective way of meeting the nation’s revenue obligations without harming other public policy goals.

As you would expect, Keynesians and supply-siders disagree about which forms of tax policy are best. Keynesians, with their concern about whether consumers can really stimulate demand, prefer progressive taxes systems that increase the effective tax rate as the taxpayer’s income increases. This policy leaves those most likely to spend their money with more money to spend. For example, in 2015, U.S. taxpayers paid a 10 percent tax rate on the first $18,450 of income, but 15 percent on the next $56,450 (some income is excluded).“2015 Federal Tax Rates, Personal Exemptions, and Standard Deductions,” http://www.irs.com/articles/2015-federal-tax-rates-personal-exemptions-and-standard-deductions (March 1, 2016). The rate continues to rise, to up to 39.6 percent on any taxable income over $464,850. These brackets are somewhat distorted by the range of tax credits, deductions, and incentives the government offers, but the net effect is that the top income earners pay a greater portion of the overall income tax burden than do those at the lowest tax brackets. According to the Pew Research Center, based on tax returns in 2014, 2.7 percent of filers made more than $250,000. Those 2.7 percent of filers paid 52 percent of the income tax paid.“High income Americans pay most income taxes, but enough to be ‘fair’?” http://www.pewresearch.org/fact-tank/2016/04/13/high-income-americans-pay-most-income-taxes-but-enough-to-be-fair/ (March 1, 2016).

Supply-siders, on the other hand, prefer regressive tax systems, which lower the overall rate as individuals make more money. This does not automatically mean the wealthy pay less than the poor, simply that the percentage of their income they pay in taxes will be lower. Consider, for example, the use of excise taxes on specific goods or services as a source of revenue.“Excise tax,” https://www.irs.gov/Businesses/Small-Businesses-&-Self-Employed/Excise-Tax (March 1, 2016). Sometimes called “sin taxes” because they tend to be applied to goods like alcohol, tobacco, and gasoline, excise taxes have a regressive quality, since the amount of the good purchased by the consumer, and thus the tax paid, does not increase at the same rate as income. A person who makes $250,000 per year is likely to purchase more gasoline than a person who makes $50,000 per year (Figure). But the higher earner is not likely to purchase five times more gasoline, which means the proportion of his or her income paid out in gasoline taxes is less than the proportion for a lower-earning individual.

Another example of a regressive tax paid by most U.S. workers is the payroll tax that funds Social Security. While workers contribute 7.65 percent of their income to pay for Social Security and their employers pay a matching amount, in 2015, the payroll tax was applied to only the first $118,500 of income. Individuals who earned more than that, or who made money from other sources like investments, saw their overall tax rate fall as their income increased.

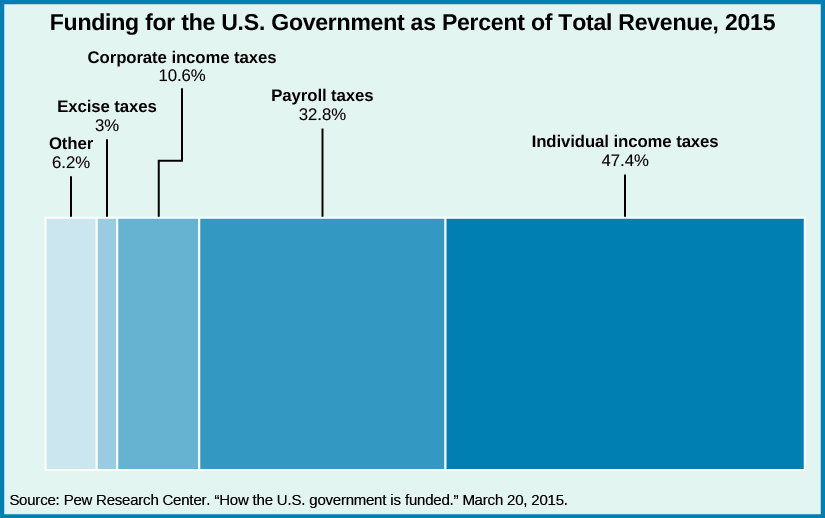

In 2015, the United States raised about $3.2 trillion in revenue. Income taxes ($1.54 trillion), payroll taxes on Social Security and Medicare ($1.07 trillion), and excise taxes ($98 billion) make up three of the largest sources of revenue for the federal government. When combined with corporate income taxes ($344 billion), these four tax streams make up about 95 percent of total government revenue. The balance of revenue is split nearly evenly between revenues from the Federal Reserve and a mix of revenues from import tariffs, estate and gift taxes, and various fees or fines paid to the government (Figure).